German Inheritance Tax for U.S. Heirs

Why It Is Not “Just a U.S. Problem”

If you live in the United States and inherit money or property from a relative in Germany – you may assume taxes are handled in America.

They are not.

Germany has its own inheritance tax.

It applies to U.S. heirs.

It can reach 30% – or higher.

And it must be reported to the German tax office, often within three months of the death.

Most U.S. heirs learn this too late.

Before you assume you owe nothing, you need to understand how German inheritance tax actually works.

1️⃣ Germany Taxes the Inheritance – Not Just the Estate

In the United States, estate tax is paid by the estate before assets are distributed.

Germany works differently.

Under the German Inheritance and Gift Tax Act (Erbschaftsteuergesetz, ErbStG), the tax is assessed on each heir individually – based on what they receive and their relationship to the deceased.

This means:

- The tax follows the heir, not just the estate

- Each heir has their own tax-free allowance

- Each heir files separately with the German tax office (Finanzamt)

- U.S. heirs are not exempt simply because they live abroad

If the deceased was a German resident at the time of death, every heir – regardless of where they live – can be subject to German inheritance tax.

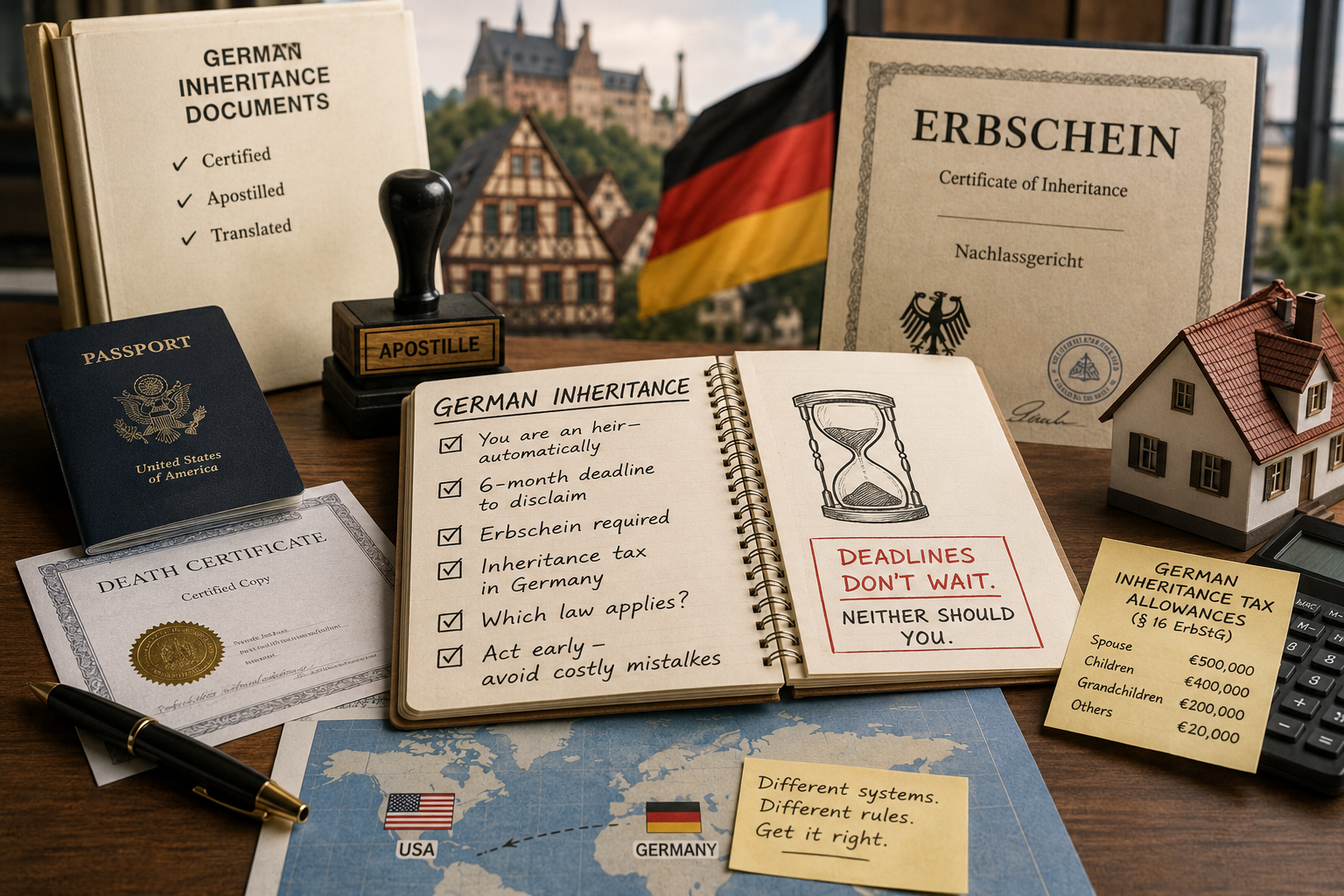

2️⃣ Your Tax-Free Allowance Depends on Your Relationship

Not everyone is taxed equally.

German law grants each heir a personal tax-free allowance (persönlicher Freibetrag) under § 16 ErbStG. The closer the family relationship, the higher the allowance.

Here is what that looks like in practice:

- Spouse or registered partner – €500,000

- Child – €400,000

- Grandchild – €200,000

- Parent (inheriting from a child) – €100,000

- Sibling, niece, nephew, or other relative – €20,000

- Unrelated heir (friend, partner, colleague) – €20,000

Only the amount above your allowance is taxed.

But there is a catch.

Any gifts received from the same person within the ten years before their death count against your allowance. A gift of €300,000 three years ago reduces your remaining allowance today.

3️⃣ The Tax Rates Can Be Steep

Once your allowance is used up, the remaining amount is taxed at progressive rates.

The rates depend on two things: the size of the inheritance and your Steuerklasse – your tax class.

Germany divides heirs into three tax classes:

- Steuerklasse I – spouses, children, grandchildren, parents

- Steuerklasse II – siblings, nieces and nephews, step-children

- Steuerklasse III – everyone else, including unrelated U.S. heirs

For Steuerklasse I, rates begin at 7% and rise to 30% for large inheritances.

For Steuerklasse III, the minimum rate is 30% – and it rises to 50% above €26 million.

A U.S. friend or distant relative inheriting €100,000 from a German resident faces a €20,000 allowance, a €80,000 taxable base, and a 30% tax bill of €24,000.

There is no paperwork that makes this go away.

4️⃣ There Is No Tax Treaty Between the U.S. and Germany

This is the part most people do not know.

The United States and Germany had an estate and gift tax treaty. It was terminated in 2000. It has never been replaced.

There is currently no bilateral agreement to prevent double taxation on inheritances between Germany and the United States.

That means:

- German inheritance tax is owed to Germany

- U.S. estate tax – where applicable – is owed to the U.S.

- The two systems do not coordinate automatically

- A foreign tax credit under U.S. law (§ 2014 IRC) may help, but only where U.S. estate tax is also due – which, given the current federal exemption of over $13 million, applies to very few estates

For most U.S. heirs, German inheritance tax is simply an additional cost with no U.S. offset.

5️⃣ You Must Report the Inheritance Within Three Months

German inheritance tax is self-reported – but the timeline is strict.

Under § 30 ErbStG, every heir must notify the German tax office (Finanzamt) of the inheritance within three months of learning of it.

This applies even if:

- You believe you owe no tax

- The estate is still in probate

- You have not yet received any assets

- You live in the United States

Failing to notify the Finanzamt on time can result in interest, penalties, and complications when you later try to access or transfer the assets.

After notification, the tax office will typically request a formal inheritance tax return (Erbschaftsteuerklärung) with documentation of all assets and their values as of the date of death.

German real estate requires a formal valuation under the Bewertungsgesetz (BewG). Bank accounts and securities are valued at the date-of-death balance.

What You Should Do Now

If you have recently inherited assets in Germany – or if you are planning ahead – here are the immediate steps that matter:

- Identify all German assets: real estate, bank accounts, securities, business interests

- Determine where the deceased was tax-resident at the time of death

- Calculate your applicable allowance and estimate taxable value

- Meet the three-month reporting deadline

- Assess any interaction with U.S. estate tax and available credits

German inheritance tax issues can be resolved – but they require timely action.

We Can Help

Our office advises U.S. clients on German inheritance tax obligations from the initial notification through the Erbschaftsteuerklärung – and we coordinate with German tax advisors on valuation and payment.

If you have questions about a German inheritance, we are ready to help.

This article is for informational purposes only and does not constitute legal advice. Inheritance tax situations are highly fact-specific. Please consult a qualified attorney before taking any action.

{kind=link}

{kind=link}

{kind=link}

{kind=link}