When Does German Inheritance Tax Reach U.S. Heirs? A Practitioner’s Overview

Many of my U.S.-based clients are surprised to learn that Germany may tax their inheritance even when the heir has never lived in Germany, holds no German passport, and receives only a fraction of an estate located overseas. The exposure to German Erbschaftsteuer is wider than most expect, and the planning window often closes quickly once the Erbfall (the moment of death) has occurred.

In my new video — released today on YouTube — I address the three threshold questions that every cross-border heir needs to work through before any distribution is made.

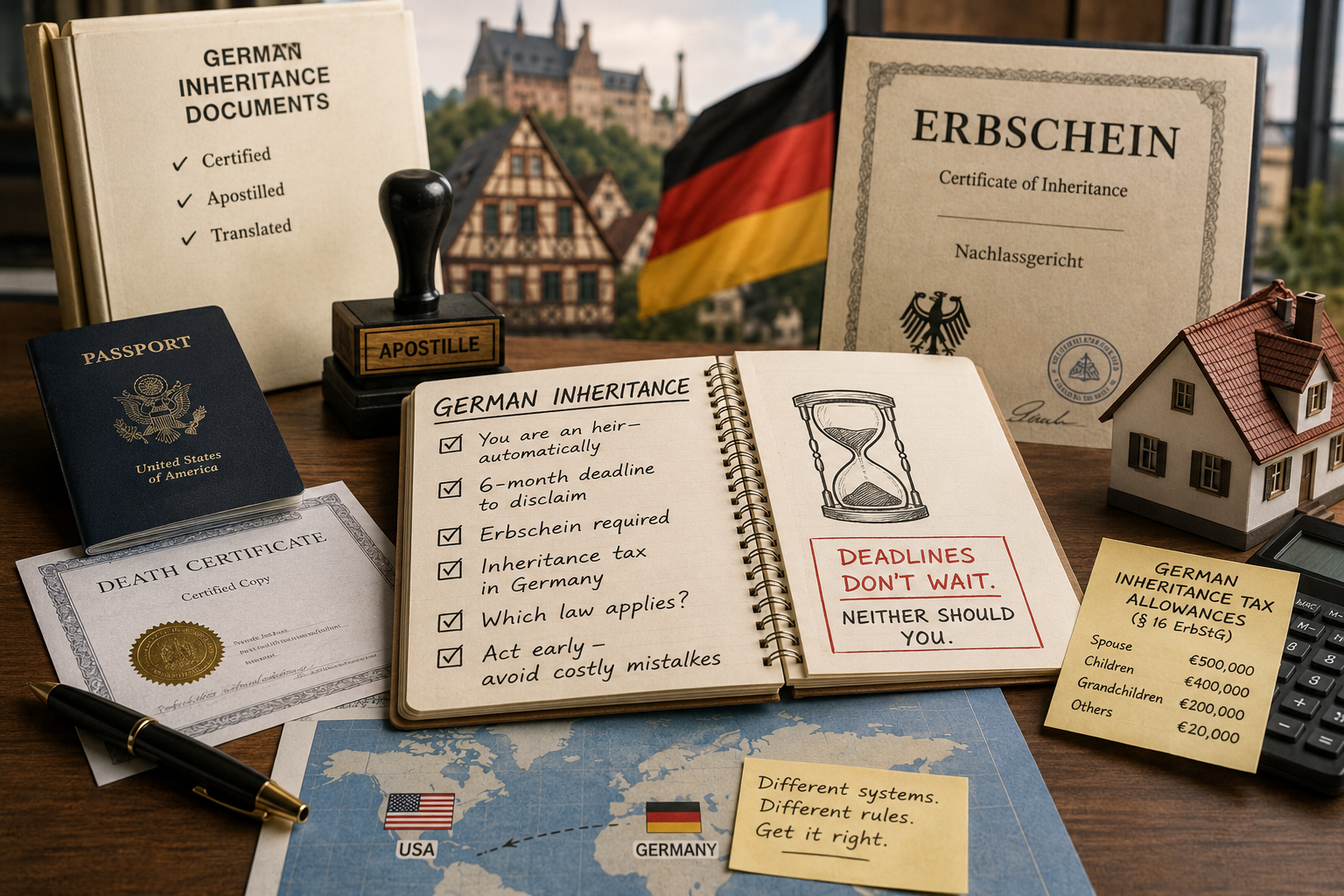

1. Does German inheritance tax apply at all? The German Erbschaftsteuergesetz (ErbStG) distinguishes between unlimited tax liability (§ 2 (1) No. 1 ErbStG), which attaches to the worldwide estate whenever either the decedent or the heir qualifies as an Inländer, and limited tax liability (§ 2 (1) No. 3 ErbStG), which captures only German-situs assets (Inlandsvermögen under § 121 BewG) — real property in Germany, shareholdings of 10 % or more in German corporations, business assets of a German permanent establishment, and similar categories. A U.S. heir of a U.S.-resident decedent can therefore still face German tax on a Frankfurt apartment or a Munich brokerage holding.

2. Which tax class (Steuerklasse) applies? § 15 ErbStG sorts beneficiaries into three classes based on relationship to the decedent. Spouses, children, and grandchildren fall into Class I; siblings, nieces, and nephews into Class II; unrelated heirs into Class III. The classification controls both the personal allowance and the marginal rate, which under § 19 ErbStG runs from 7 % to 50 %.

3. How much is exempt? The personal allowances under § 16 ErbStG are generous by international standards — €500,000 for spouses, €400,000 per child, €200,000 per grandchild — but for non-resident constellations they must be read together with § 16 (2) ErbStG, which prorates the allowance based on the ratio of German-situs to worldwide estate value. The 2017 reform (in response to the ECJ’s Hünnebeck and Welte decisions) modernized this rule but did not eliminate the trap.

The video walks through these provisions with examples drawn from common U.S.–Germany fact patterns. If you are administering or expecting a German inheritance, I would encourage you to watch the full video and reach out for a tailored analysis.

▶ Watch the full video: https://www.youtube.com/watch?v=wyZxliiepb0

{kind=link}

{kind=link}

{kind=link}

{kind=link}