If you are an American who has just learned you stand to inherit property, a bank account, or a family home in Germany, your first instinct may be to wait until things „settle down.“ In a German estate, waiting can be the most expensive decision you make. The German system runs on its own rules, its own deadlines, and its own paperwork — and almost none of it works the way probate does in the United States.

Here is what every U.S. heir should understand from the start.

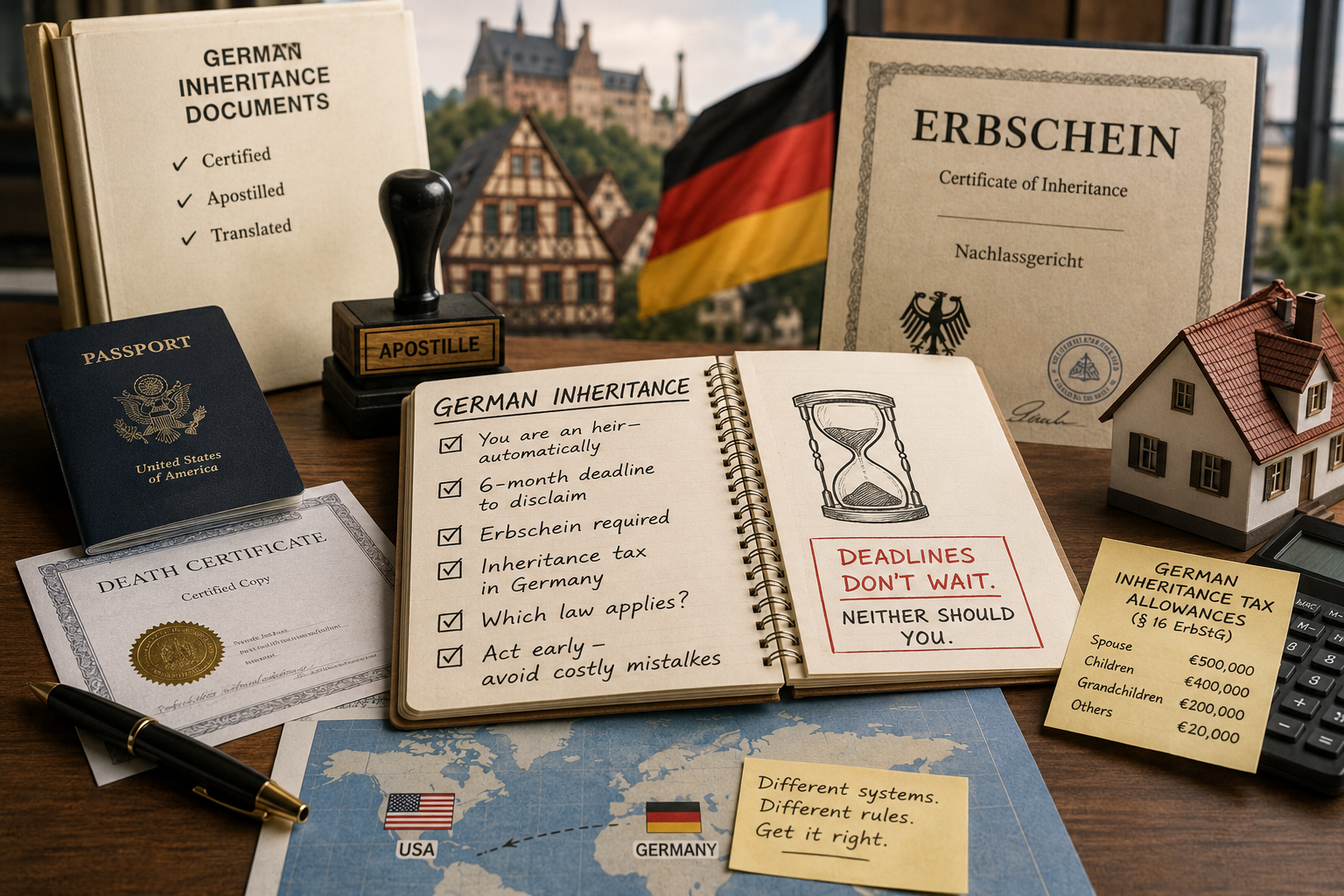

You may already be an heir — automatically

Unlike in the U.S., a German estate does not pass through a court-supervised probate administrator. Under German law (§ 1922 BGB), the estate passes to the heirs directly and immediately at the moment of death — assets *and* debts. There is no waiting room. If the deceased left more debt than value, you generally have only a limited window to formally disclaim the inheritance (the *Ausschlagung*): six weeks if you are in Germany, but six months if you live abroad (§ 1944 BGB). Miss that window, and you may inherit the debts along with the assets.

You will likely need an Erbschein

To actually access a German bank account or transfer real estate into your name, German institutions will usually require an Erbschein — a certificate of inheritance issued by the local probate court (Nachlassgericht). Getting one as an overseas heir involves documentation that often surprises American families: certified records, sworn statements, and frequently apostilled and translated U.S. documents such as death certificates or marriage records. This takes time, and starting early matters.

German inheritance tax is separate from U.S. estate tax

Germany levies inheritance tax (Erbschaftsteuer) on the heir, not on the estate, and the tax-free allowances depend on your relationship to the deceased (§ 16 ErbStG):

– Spouses: €500,000

– Children:€400,000

– Grandchildren:€200,000

– Everyone else (e.g., siblings, nieces, nephews, friends): €20,000

A U.S. heir can owe German inheritance tax even while living entirely in the United States, if German-situated assets are involved. The tax office (Finanzamt) must generally be notified within three months of becoming aware of the inheritance (§ 30 ErbStG). Because the U.S. has no inheritance tax of its own and the two systems are not mirror images, careful coordination is essential to avoid paying more than you owe.

Which country’s law even applies?

Since the EU Succession Regulation, the law governing a cross-border estate generally follows the deceased’s last habitual residence — though a valid choice of law in a will can change that. For German-American families, this single question often determines who inherits, in what shares, and whether forced-heirship rules (Pflichtteil) come into play.

The takeaway

A German inheritance is rarely a simple matter of „claiming“ what is yours. Between strict deadlines, court certificates, document legalization, and a tax authority on a different continent, small early missteps can become costly. If you have learned you may inherit in Germany, the smartest first step is to map out the deadlines and requirements before the clock runs out.

—

This article is general information on German inheritance law and not legal advice for any specific situation. Cross-border estates turn on their particular facts. If you are facing a German-American inheritance matter, I am happy to help you assess your position.

{kind=link}

{kind=link}

{kind=link}

{kind=link}